|

时间序列

在一个时间段中不同时刻得到的数据,一般有的是固定频率(比如每小时)。这里要介绍的内容主要包括三部分:

1.Timestamps, specific instants

in time

2.Fixed periods, such as the

August of 2014

3.Intervals of time, indicated

by a start and end timestamp

用到的工具主要就是 Pandas 了。

相关工具

和时间相关的几个modules主要有 datetime, time 和 calendar

In

[317]: from datetime import datetime

In [318]: now = datetime.now()

In [319]: now

Out[319]: datetime.datetime(2012, 8, 4, 17,

9, 21, 832092)

In [320]: now.year, now.month, now.day

Out[320]: (2012, 8, 4) |

datetime objects 和 string 之间的转换

datetime

objects转string

In [9]: stamp = datetime(2011, 1, 3)

In [10]: str(stamp) 或者 stamp.strftime('%Y-%m-

%d')

Out[10]: '2011-01- 03' |

string

转 datetime

In [332]: value = '2011-01-03'

In [333]: datetime.strptime(value, '%Y-%m-%d')

Out[333]: datetime.datetime(2011, 1, 3, 0,

0)

In [334]: datestrs = ['7/6/2011', '8/6/2011']

In [335]: [datetime.strptime(x, '%m/%d/%Y')

for x in datestrs]

Out[335]: [datetime.datetime(2011, 7, 6, 0,

0), datetime.datetime(2011, 8, 6, 0, 0)] |

还可以调用parser.parse来自动解析时间

In

[336]: from dateutil.parser import parse

In [337]: parse('2011-01-03')

Out[337]: datetime.datetime(2011, 1, 3, 0,

0)

dateutil 可以解析绝大多是时间的表达式

>In [338]: parse('Jan 31, 1997 10:45 PM')

Out[338]: datetime.datetime(1997, 1, 31,

22, 45)

国际上,一般先写日子再写月份

In [339]: parse('6/12/2011', dayfirst=True)

Out[339]: datetime.datetime(2011, 12, 6,

0, 0) |

Pandas的应用

Pandas 是设计用来处理 arrays of dates的,作为DataFrame当中的axis

index或者 column.

to_datetime 方法用于解析许多不同类别的日期表达式。

In

[340]: datestrs

Out[340]: ['7/6/2011', '8/6/2011']

In [341]: pd.to_datetime(datestrs)

Out[341]:

<class 'pandas.tseries.index.DatetimeIndex'>

[2011-07-06 00:00:00, 2011-08-06 00:00:00]

Length: 2, Freq: None, Timezone: None |

to_datetime 还可以处理 the values that should be considered

missing (None, empty string, etc.):

In

[342]: idx = pd.to_datetime(datestrs + [None])

In [343]: idx

Out[343]:

<class 'pandas.tseries.index.DatetimeIndex'>

[2011-07-06 00:00:00, ..., NaT]

Length: 3, Freq: None, Timezone: None

In [344]: idx[2] #最后加上去的[None]

Out[344]: NaT

In [345]: pd.isnull(idx)

Out[345]: array([False, False, True], dtype=bool)

NaT (Not a Time) is pandas’s NA value for

timestamp data. |

Series 基础

在pandas中最基本的时间序列文件是 a Series indexed by timestamps

In

[346]: from datetime import datetime , from

pandas import *

In [347]: dates = [datetime(2011, 1, 2), datetime(2011,

1, 5), datetime(2011, 1, 7),datetime(2011,

1, 8), datetime(2011, 1, 10), datetime(2011,

1, 12)]

In [348]: ts = Series(np.random.randn(6),

index=dates)

In [349]: ts

Out[349]: # 以时间作为index,一列是6位的随机数

2011-01-02 0.690002

2011-01-05 1.001543

2011-01-07 -0.503087

2011-01-08 -0.622274

2011-01-10 -0.921169

2011-01-12 -0.726213 |

之前的变量变成 TimeSeries了,并且是DatetimeIndex

In

[350]: type(ts)

Out[350]: pandas.core.series.TimeSeries

In [351]: ts.index

Out[351]:

<class 'pandas.tseries.index.DatetimeIndex'>

[2011-01-02 00:00:00, ..., 2011-01-12 00:00:00]

Length: 6, Freq: None, Timezone: None |

和其他Series一样,differently-indexed time series的算数操作是对齐时间的。

先复习一下:

ts[::2]是每间隔两个取数据,ts[:2]是去其前两个数据

In [45]: ts[::2]

Out[45]: 2011-01-02 0.040974

2011-01-07 -0.687850

2011-01-10 -1.862041

dtype: float64

In [352]: ts + ts[::2]

Out[352]:

2011-01-02 1.380004

2011-01-05 NaN

2011-01-07 -1.006175

2011-01-08 NaN

2011-01-10 -1.842337

2011-01-12 NaN |

Date Ranges, Frequencies, and Shifting

时间序列数据经常要根据时间的频率(像每小时、每天、每月……)来使用。

用 resample 来完成这一点:

In

[349]: ts

Out[349]:

2011-01-02 0.690002

2011-01-05 1.001543

2011-01-07 -0.503087

2011-01-08 -0.622274

2011-01-10 -0.921169

2011-01-12 -0.726213

In [24]:

ts.resample('D') # 按每天的数据排列,缺省值用NaN代替

Out[24]:

2011-01-02 1.242749

2011-01-03 NaN

2011-01-04 NaN

2011-01-05 -2.575903

2011-01-06 NaN

2011-01-07 0.375028

2011-01-08 0.636902

2011-01-09 NaN

2011-01-10 1.544629

2011-01-11 NaN

2011-01-12 -0.033450

Freq: D, dtype: float64 |

产生时间范围,默认的 date_range 产生daily timestamps

In

[382]: index = pd.date_range('4/1/2012', '6/1/2012')

In [383]: index

Out[383]:

<class 'pandas.tseries.index.DatetimeIndex'>

[2012-04-01 00:00:00, ..., 2012-06-01 00:00:00]

Length: 62, Freq: D, Timezone: None |

再看一下Shift data. 就是将Data在时间轴上移来移去。

##

Timestamps 不变,“shift 2”把数据往后移两天, 超过范围的就discarded了,

缺少的用NaN代替

In [399]: ts = Series(np.random.randn(4),index=pd.date_range('1/1/2000',

periods=4, freq='M'))

In [400]: ts In [401]: ts.shift(2) In [402]:

ts.shift(-2)

Out[400]: Out[401]: Out[402]:

2000-01-31 0.575283 2000-01-31 NaN 2000-01-31

1.814582

2000-02-29 0.304205 2000-02-29 NaN 2000-02-29

1.634858

2000-03-31 1.814582 2000-03-31 0.575283

2000-03-31 NaN

2000-04-30 1.634858 2000-04-30 0.304205

2000-04-30 NaN

Freq: M Freq: M Freq: M |

一个常用的就是算每一步的增长率了

Share Prices

时间序列的绘图

导入几只股票的价格数据

In

[539]: close_px_all = pd.read_csv('ch09/stock_px.csv',

parse_dates=True, index_col=0)

In [540]: close_px = close_px_all[['AAPL',

'MSFT', 'XOM']]

In [541]: close_px = close_px.resample('B',

fill_method='ffill')

In [542]: close_px

Out[542]:

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 2292 entries, 2003-01-02 00:00:00

to 2011-10-14 00:00:00

Freq: B

Data columns:

AAPL 2292 non-null values

MSFT 2292 non-null values

XOM 2292 non-null values

dtypes: float64(3) |

对其中任意一列调用plot生成简单图表

| In

[544]: close_px['AAPL'].plot() |

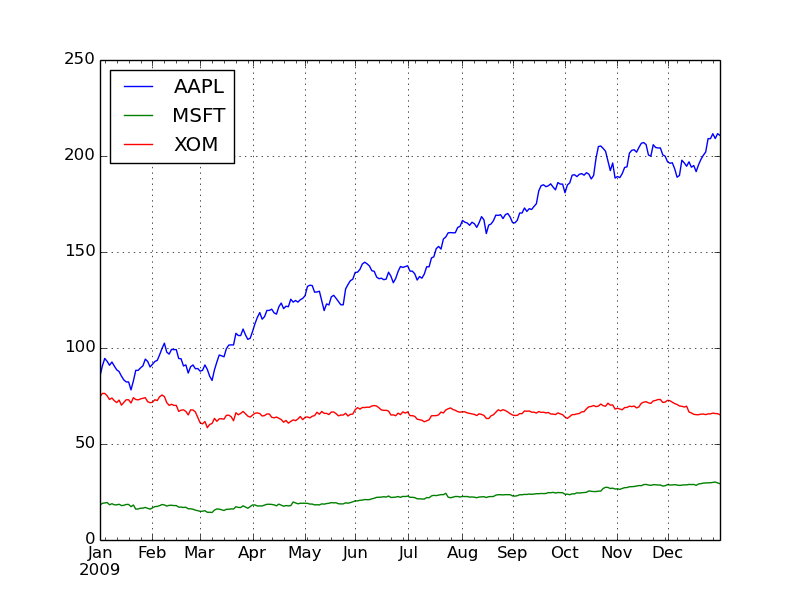

对DataFrame调用plot时,所有时间序列被绘制在一个subplot上

| In

[544]: close_ix['2009'].plot() |

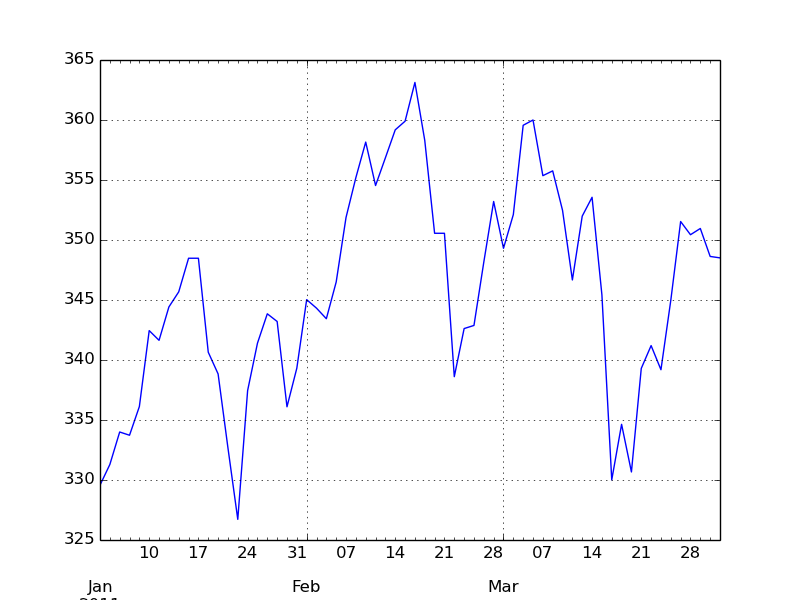

来看看Apple的股价

from January to March

| In

[548]: close_px['AAPL'].ix['01-2011':'03-2011'].plot()

|

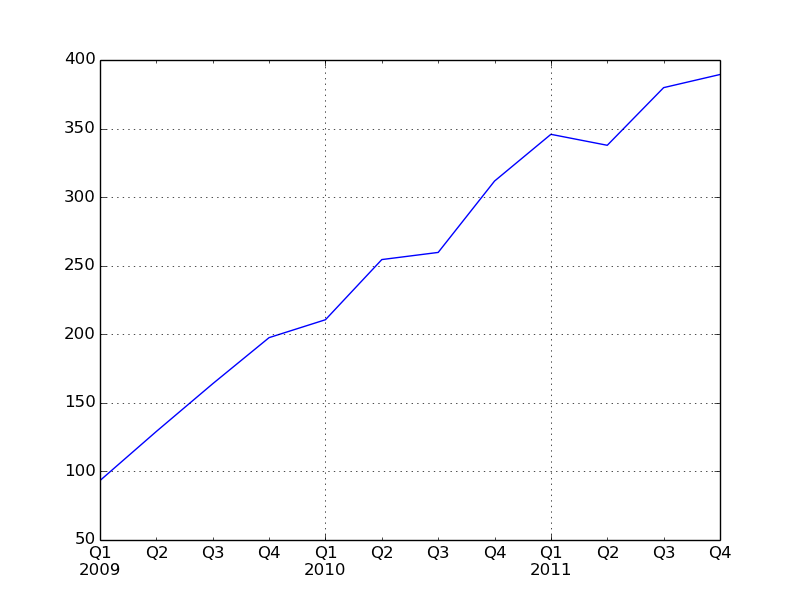

用季度型频率的数据会用季度标识进行格式化

In

[550]: appl_q = close_px['AAPL'].resample('Q-DEC',

fill_method='ffill')

In [551]: appl_q.ix['2009':].plot() |

|